Table of Content

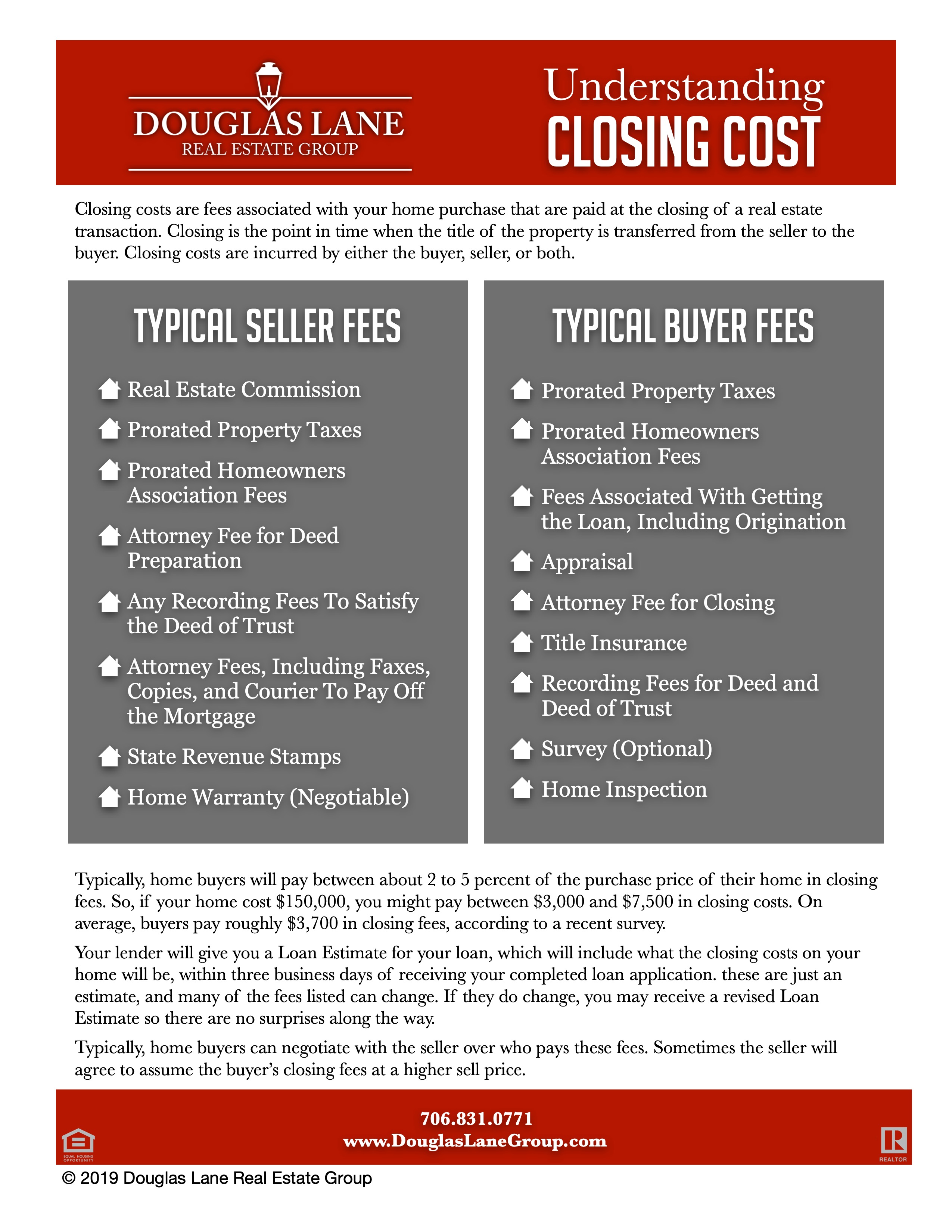

We track the cost of each fee by city and state to give you the best estimate on closing costs. For example, they include the cost of the home appraisal and home title searches that lenders require. A more detailed list of closing costs appears below, and your real estate agent can help estimate yours for your area and loan type. Your lender will also tell you what you can expect to pay at closing after you apply for a mortgage, in a document called a Loan Estimate. At closing, buyers are often required to open an ongoing escrow account from which their mortgage servicer will pay ongoing costs. An escrow account is free to open or maintain because it’s a requirement for loans with less than 20% down.

Many of the closing costs you’ll pay as a buyer are related to the opening of your mortgage. Closing costs can vary significantly based on the type of loan you choose. Here’s a quick summary of what you can expect to pay, based on loan type.

Appraisal

Your property taxes will be prorated based on your closing date. Some buyers pay their taxes in lump sums annually or biannually. If you don’t pay this way, you might escrow the taxes, which means they would be included as an escrow line item in your monthly mortgage payment to your loan servicer. Typically optional for buyers, owner’s title insurance protects you from future claims against the title. The seller typically pays for the owner’s policy, but this needs to be negotiated and detailed in the purchase and sale contract. Owner’s title insurance policies range from $500 to $3,500 depending on the location and size of the property.

Lender credits represent money the lender provides to cover closing costs upfront. Depending on where you live, first-time homebuyer programs are available to help you pay for closing costs. Many housing finance agencies offer some form of down payment and closing cost assistance to qualified buyers who meet income and purchase price requirements. As the seller, you’ll also need to bring a little cash to the closing table to finish out the loan. Let’s take a look at some common closing costs sellers must pay to finalize a home sale. Property taxes are fees that you pay to your local government in exchange for public services.

things to know about a Closing Disclosure

Real estate attorney charges depend on your state and local rates. Closing costs are paid according to the terms of the purchase contract made between the buyer and seller. Usually the buyer pays for most of the closing costs, but there are instances when the seller may have to pay some fees at closing too. All these factors make it very difficult to accurately determine closing costs, however, the average total closing costs for most buyers is 2% to 5% of the loan amount.

Similar to an FHA loan, there are limits to how much of the buyer’s closing costs the seller can cover. If you make a down payment of 25% of the purchase price or more, the seller can pay for closing costs up to 9% of the total loan amount. If your down payment is between 10% and 24%, they can cover up to 6%. For down payments of less than 10%, the seller can assist with closing costs up to a total of 3% of the loan amount. As a buyer, you can request that the seller pay for some or all of your closing costs while negotiating the offer. According to the Zillow Group Consumer Housing Trends Report 2020, 85% of sellers make some kind of trade-off with the buyer to facilitate the sale of a home.

Ask The Seller To Contribute

Out of that total commission amount, the seller also usually pays the buyer’s agent commission , which is generally 2-3% of the total amount offered. Lenders often charge an underwriting fee, which covers the cost of researching whether or not they should approve you for a loan. If it is charged separately, it can range between $400 and $900.

A surveyor will verify all property lines and evaluate things like shared fences. The buyer typically pays this fee, though you may be able to negotiate the cost with the seller. On average, the survey costs around $500, with larger lots costing more. As the buyer, you can’t have the seller pay more than 4% of the total loan amount in closing costs.

This won’t avoid or reduce costs, but it will mean you can pay them off over time, instead of in one big lump sum on closing day. One of the little-known facts that can save you some money is that by scheduling your closing date near to or right at the end of the month can reduce daily interest rate charges. While this isn’t a huge amount, it all adds up, so it’s worth checking with your lender to see how changing your closing date could help you save on closing costs. It’s a free market and rates are not consistent from lender to lender, or from service to service.

Finder.com compares a wide range of products, providers and services but we don't provide information on all available products, providers or services. Please appreciate that there may be other options available to you than the products, providers or services covered by our service. You may also be able to find programs for forgivable grants, deferred payment second mortgages and fully amortizing second loans. Down payment assistance programs are often targeted toward certain groups, such as first-time homebuyers, active military members, veterans or teachers. Once the sale is official and the title is transferred from the previous owner to the new owner , taxes on the transaction are required to be paid as well. In some states the law requires that an attorney is present at the closing.

We do not manage client funds or hold custody of assets, we help users connect with relevant financial advisors. A financial advisor can help you create a financial plan for your home buying goals. To find a financial advisor who serves your area, try our free online matching tool. Programs, rates, terms and conditions are subject to change without notice. We ask for your email address so that we can contact you in the event we're unable to reach you by phone.

Buyers and sellers each pay unique closing costs to finalize a home sale. In Kentucky, sellers typically pay for the title and closing service fees, transfer taxes, and recording fees at closing. Optional costs for sellers include buyer incentives, pro-rated property taxes, or for an attorney. We include every possible fee that you could be charged when closing a home, including title insurance, inspection fees, appraisal fees and transfer taxes. In fact, we replicate an entire Loan Estimate that you would get from a potential lender for your specific area.

At closing, you may also make your first HOA dues payment, prorated based on your closing date. Escrow fees range depending on your location, but are typically about 1% of the home sale price. The cost is typically split evenly between the buyer and seller, but this must be negotiated and detailed in the contract. This does not occur on all loans during underwriting, but sometimes the initial report occurred in the month prior to closing, and your lender may require a more recent report. The calculator’s default setting offers estimates for many of the closing costs. If you know the cost for an item, enter it in the calculator to improve the results.

No comments:

Post a Comment